May Recap and June Outlook

The Fed lion has found the courage to increase interest rates drastically, the inflation tiger is still ambushing the economy, and now the stock market is flirting with bears. The question for investors is: Are we still deep in the forest? Or is that the Emerald City on the horizon? To extend the metaphor – that wizard wasn’t much help, and the solution to the problem turned out to be a liquidation.

Just to be clear, they melted the witch. We’re not suggesting melting your portfolio.

Let’s recap the recent data releases as we head into the big one – May inflation – which will be released on June 10th

- The National Association for Business Economics reported a lower projection for GDP.

- The survey also addressed respondents’ outlook on recession. More than half (53%) of respondents assign a more than 25% probability of a recession occurring within 12 months.

- The Bureau of Labor Statistics released the May non-farm payrolls on June 3rd. The economy beat expectations and created 390,000 jobs. That is definitely not very recession like.

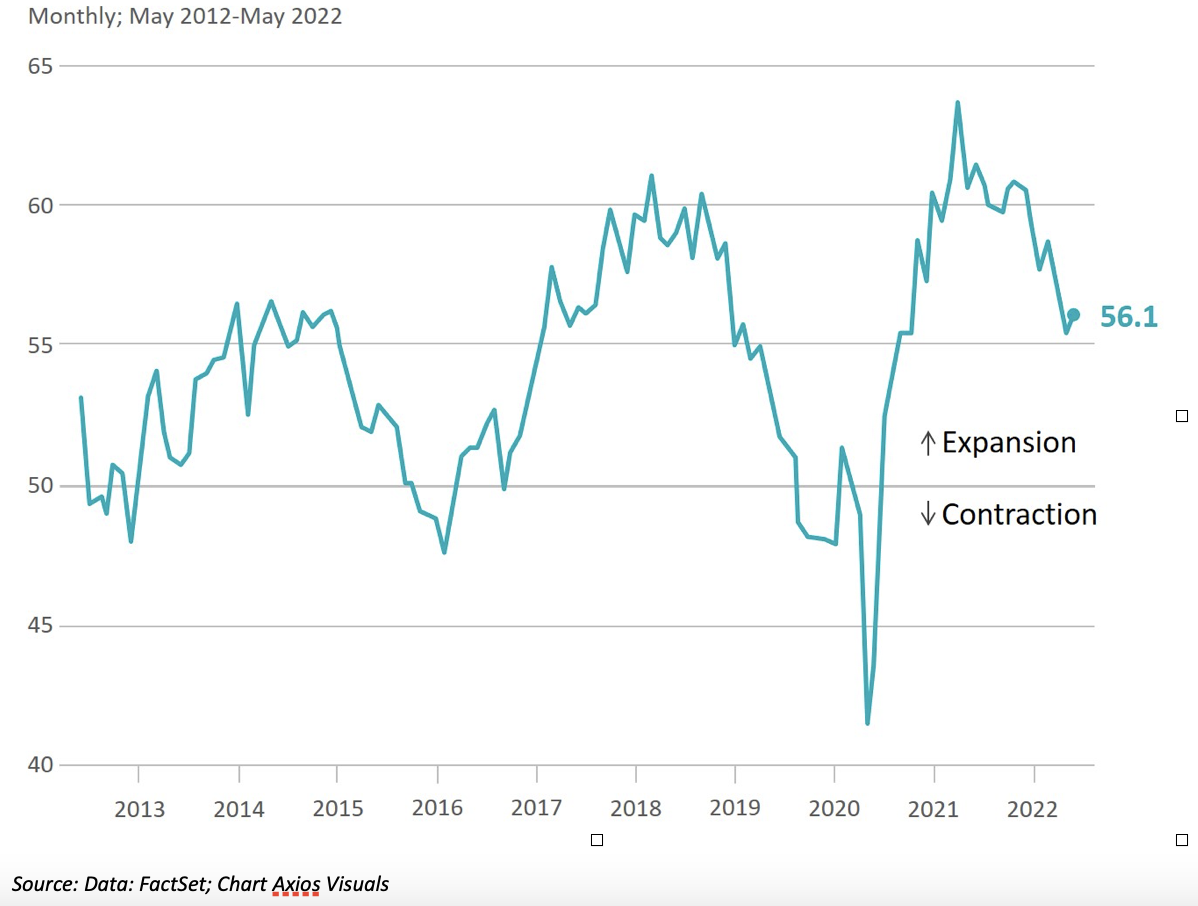

- A key manufacturing sector index is still positive. The Institute for Supply Management Purchasing Managers’ Index for May was 56.1. Any number above 50 indicates expansion, while numbers below 50 show shrinkage.

- And consumers are still spending. The Conference Board said on May 31st that its consumer confidence index dipped to 106.4 in May, from 108.6 in April. This is still a strong reading.

What Does All of That Data Add Up To?

The Fed is trying to contain inflation by slowing economic growth. The key inputs are consumer demand for goods, which of course, is driven by strength in consumer balance sheets. And that is driven by full employment and rising wages. The Fed is increasing interest rates, which makes money more expensive.

- Business investment depends on access to capital. Less capital means less growth and fewer jobs.

- Mortgage rates have increased more than 200 basis points. This has already slowed the booming housing market, which will have a knock-on effect on several job sectors.

- Consumer credit is more expensive, which should result in a slowdown in consumer demand.

The Fed is aggressively raising rates at a stated – and unusual — pace of 50 basis points at each of the next several meetings. Even before rates go up, the market begins to price in where rates will be months down the road.

That’s part of what is contributing to the pullback in equities we’ve seen this year. The market is also reacting to uncertainty. There’s no way to know if the Fed will be successful.

Lowering Inflation Requires Slowing Economic Growth – But How Slow Is Too Slow?

The Fed’s stated belief is that the long-term potential growth rate of the U.S. is around 1.8%. Growth at this level would be likely to keep inflation at the Fed’s preferred level of approximately 2%.

How Did the Markets React?

After tickling the bear mid-month, the S&P 500 managed to close in positive territory by a hair of 0.01%. After seven consecutive weeks of declines, the index saw the best weekly performance since November 2020.

All eyes are on inflation. After declining slightly last month, markets will be looking for more evidence that the Fed’s aggressive rate moves are working. Gas prices have bounced back up to levels not seen since the first weeks of the Ukraine invasion. Headline CPI includes energy – so the pressure is on.

It’s probably hard to understate the impact of the inflation number as a market mover. The belief that the Fed would need to be even more aggressive in raising rates – with a potential 75 basis point increase – was in part responsible for the sustained negativity about equity markets. With even a small decrease in inflation, market sentiment moved back to positive as investors displayed more confidence that rate increases would be at the levels the Fed has outlined.

Chart of the Month: Manufacturing is Still Expanding

Institute for Supply Management – Purchasing Managers Index

Source: Data: FactSet; Chart Axios Visuals

Equity Markets

- The S&P 500 was up 0.01% in May, bringing its YTD return to -13.30%

- The Dow Jones Industrial Average gained 0.04% for the month and returned -9.21% YTD

- The S&P Mid-Cap 400 increased 0.58% for the month resulting in a -11.51% YTD return

- The S&P Small-Cap 600 declined 1.72% in April, putting the YTD return at -11.85%

Source: All performance as of May 31st, 2022; quoted from S&P Dow Jones Indices.

The Q1 2022 earnings season is mostly complete, with over 97% of companies reporting. Of 489 issues, 377 beat operating estimates (77.1%), while 350 of the 486 (72.0%) have beaten estimates on sales. The quarter is expected to decline 12.7% from the Q4 2021 record and be up 4.4% over Q1 2021. For 2022, earnings are expected to set another record, increasing 7.5% over 2021.

Bond Markets

- The 10-year U.S. Treasury ended the month at 2.85%. Intra month, the key rate reached 3.21%. This marks the first time this rate has been above 3% since December 2018. The Bloomberg U.S. Aggregate Index was up, returning 0.64%. As represented by the Bloomberg Municipal Bond Index, Municipal bonds returned 1.48%. High yield corporate bonds were positive, with the Bloomberg U.S. High Yield Index returning 0.24%

The Smart Investor

First, let’s look at some stats for bear markets:

- According to the Schwab Center for Financial Research, the average bear market lasts only around 15 months.

- A bear market is defined as a drop of 20% from the peak

- Bear markets are considered to be recession indicators – they begin before a recession starts, as investors become more risk-averse. “Buy the dip” becomes “Shift to cash”

- They can also simply indicate a temporary lull. That’s what happened in 2020.

The bear was definitely at the door. And he may be back, even if not to stay. The traditional course of action for a bear market is to shift to a defensive strategy and try to cushion your portfolio with more conservative investments that throw off cash. For example, bonds and dividend stocks. However, before you revamp your portfolio – consider your own goals and your plan.

Recession-proofing your entire financial plan means revisiting expenses, reviewing cash planning, understanding your interest charges, and thinking about the long-term. Timing markets isn’t a long-term strategy. It’s too easy to miss when the turn happens, and markets begin to rebound, and being out of the market can be very costly.

One more stat: Ned Davis Research finds that, on average, stocks lose around 36 percent during a bear market. Hartford Funds has the bull market stat: a 114 percent gain on average.

Please feel free to reach out with any questions you may have. Connect here

This work is powered by Seven Group under the Terms of Service and may be a derivative of the original. More information can be found here.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

This content not reviewed by FINRA