SEP vs. SIMPLE IRA for you small business? Wondering what you should do? Let’s take a closer look at options.

As a business owner, you may be searching for retirement plan options that benefit both you and your employees… all while avoiding burdensome costs and administrative complexity. If you’ve been considering 401(k)’s, you will first want to check out my post Should I Set Up A Traditional 401(k) for My Business, and then you may want to take a look at the SEP vs. SIMPLE IRA. These options offer more customized plans based on goals, preferences, business size, and contribution levels. So which plan is right for your business? Let’s take a look at them in this week’s Inside Look at Building Towards Wealth.

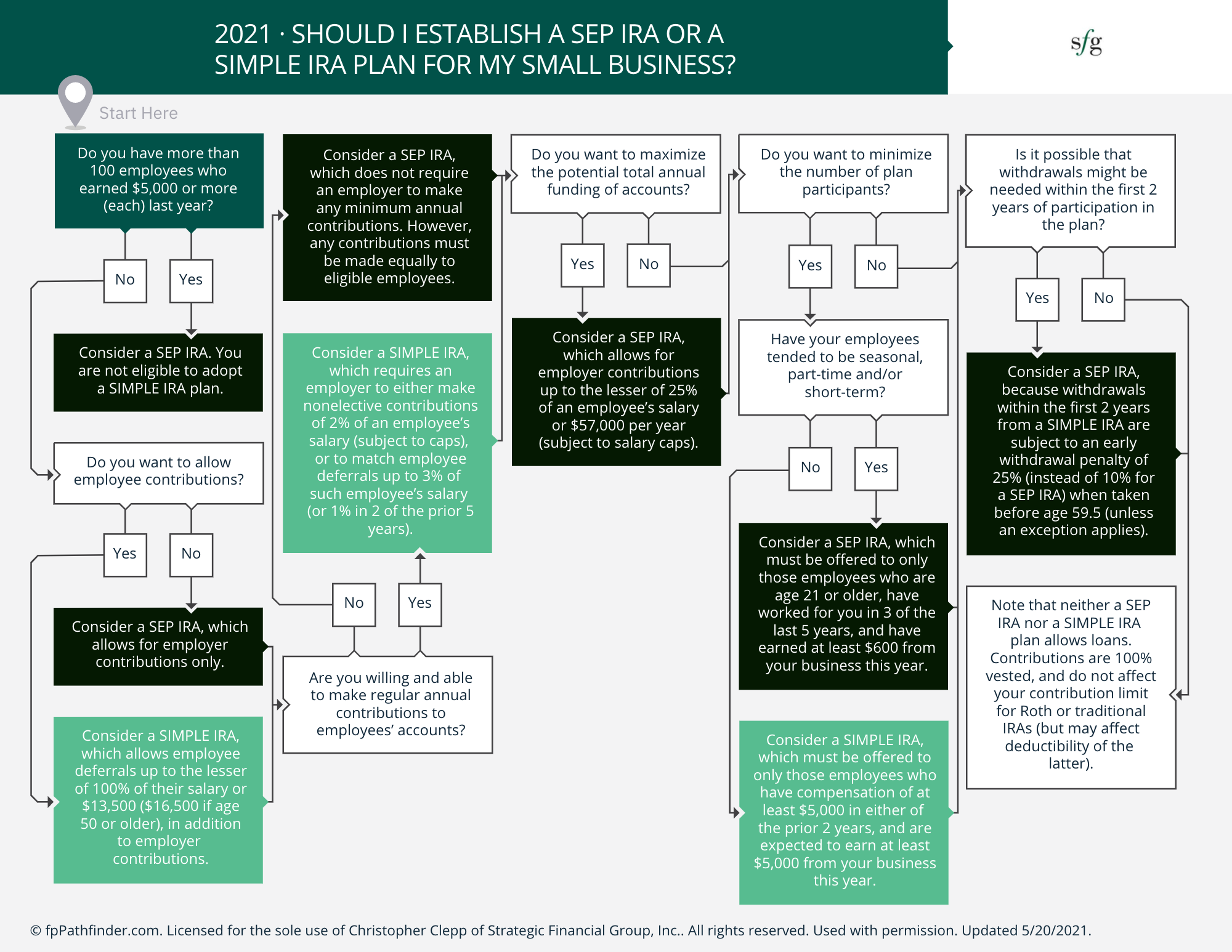

For starters, if you have over 100 employees that each make $5k or more annually, consider a SEP IRA plan; however, if you have a smaller company with lower payouts, you should consider a SIMPLE IRA plan.

If you want to solely allow employee contributions, then you should consider the SIMPLE IRA plan. Otherwise, the SEP IRA allows for employer contributions only.

Next, consider contribution frequency. Can you commit to annual contributions to employees’ accounts? If so, a SIMPLE IRA requires an employer to either

Make nonelective contributions of 2% of an employee’s salary (subject to caps) or

To match employee deferrals up to 3% of such employee’s salary (or 1% in 2 of the prior 5 years).

If this is something you’d rather steer clear from, then review the SEP IRA plan. Although you don’t have to make regular contributions, you’re still required to divide contributions equally upon eligible employees.

Likewise, if you want to maximize the potential total annual funding of accounts, then a SEP IRA may be best. This way, you can contribute up to the lesser of 25% of your employee’s salary, or $57,000 per year (subject to salary caps).

Speaking of capping out, would you prefer to minimize the total number of plan participants? There are a few things to ponder before reaching the next step. If you answered yes and your employees tend to be more short term, then you’ll want to consider the SEP IRA. If you answered yes and you’ve got long term employees, then a SIMPLE IRA may be ideal.

Lastly, if you answered no altogether, then let’s ask this question: will withdrawals be necessary within the first 2 years? If so, then consider a SEP IRA because a SIMPLE IRA can be subject to penalties in this case.

Regardless of which plan you choose for your team, neither a SEP IRA nor a SIMPLE IRA plan allows for loans. Contributions are 100% vested, and do not affect your contribution limit for Roth or Traditional IRAs (but may affect deductibility of the latter). They can be great alternatives to 401(k)’s. Which one is best is determined by your circumstances as a business owner. So, which is best for yours? If you still have questions reach out and I will be happy to help.